While buying a home, we have often heard the term Escrow from the lender or real estate agent. The term describes a few different functions from the offer acceptance day to deal close day, or even when you become the homeowner.

Eventually, two types of Escrow account are used during the home buying process. One, that is used while the home buying process and another is an impound account used for mortgage services, which helps manage property tax and insurance payments.

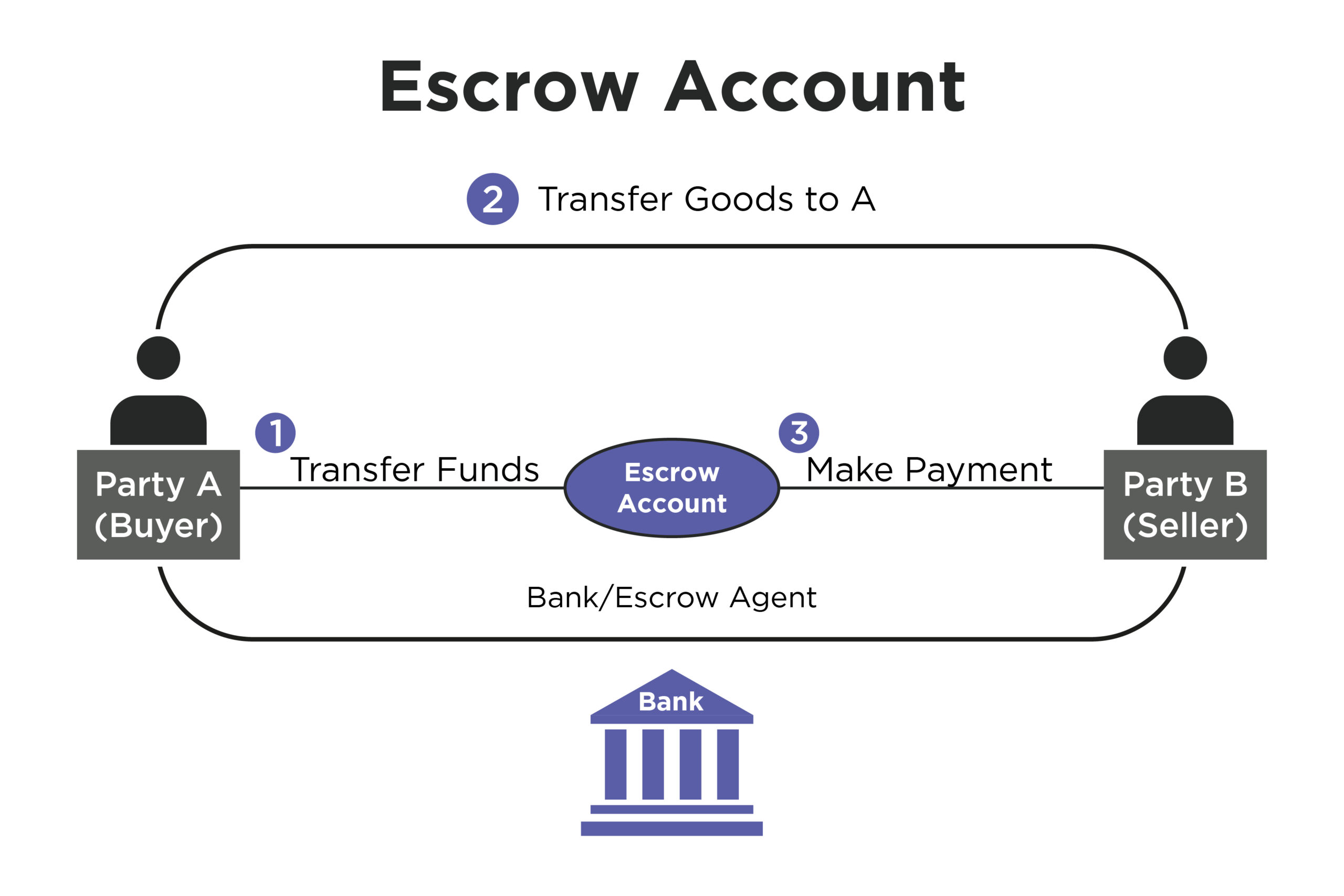

So what does an Escrow account mean?

It is a contractual arrangement that includes a neutral third party, an Escrow agent, who receives and disburses funds for transaction parties.

Typically the agent opens up an Escrow account after the seller and the buyer agrees on the home price and sign the purchase agreement.

The Escrow account serves two primary purposes:

• To hold earnest money.

• To handle and disburse the fund till the Escrow are fulfilled, and the report is dispersed.

Working on Escrow:

When an offer is made on a home, the seller has to pay earnest money, which is held in an escrow account until the deal is negotiated. It gives assurance to the seller that the buyer will not back out and get motivated to choose such offers in the future.

What is closing the Escrow?

The Escrow is closed when all the conditions are met. A home loan is received, and legally, the title has been passed. While the closing process, the transaction is disbursed to appropriate parties, ensuring that the documents are signed and a new deed is prepared to name the new owner.

After that, the Escrow officer sends the deed to county records before it is officially closed. After the closure, the buyer and the seller receive the final closing statement.

Escrow analysing statement:

Every month, the mortgage statement shows the amount accrued in the impound account. The mortgage services are sent by law to the buyers/owners every year to deliver the following Escrow account analysis.

• The fund received.

• The fund is paid as insurance and property tax.

• Estimation of Escrow portion increment and decrement based on premium owned.

• Escrow shortage (Not enough funds in the account).

• Escrow deficiency ( Negative balance of the report).